6 Things To Consider When Your Mortgage Comes Up For Renewal

It’s the perfect time to find a lower rate if you prepare ahead of time.

Wouldn’t it be nice if your mortgage had a reset button? Pressing it would let you find a new rate, change your term and find a mortgage that better suits you. Well, that button doesn’t quite exist, but a mortgage renewal gets you most of the way there.

Mortgage renewals happen at the end of your current mortgage term. The most popular mortgage term is five years, but they can range anywhere from one to 10 years. You’ll have to renew your mortgage at the end of every term until your mortgage is fully paid off. You have until the end of your amortization period (usually 25-30 years) to pay off your entire mortgage.

Advertisement

Renewal time is the best time for you to change providers to get a better rate, or refinance to get a mortgage that better suits your current needs. Here are six things that will give you the best chance at doing so successfully.

1. Evaluate your current goals

Your financial needs have probably changed since you first got your mortgage. Here are some important decision points to consider at renewal:

- Fixed or variable rate: Fixed rates stay the same for your entire mortgage term, while variable rates fluctuate throughout. Variable rates are directly tied to your lender’s prime rate. So, when your lender’s prime rate drops, you could benefit; but if they go up, so does your mortgage rate. If you want stability in your monthly payments, then fixed rates are the way to go. If you’re OK with some risk and expect rates to drop, then you might consider a variable-rate mortgage.

- Your term length: Depending on your plans and current financial situation, a new term length might suit you better. If you don’t expect any major lifestyle changes, a longer term can help you keep a great rate for longer. If you want more flexibility, go for a shorter term.

- Customer service: Are you happy with the service your current lender provides? If not, renewal time is a great opportunity to consider other providers who might better meet your needs.

- Do you need extra cash? You can access some of the equity you’ve already built into your home with a Home Equity Line of Credit (HELOC), or by refinancing. Both are powerful options, but both have some drawbacks.

2. Don’t accept your renewal offer right away

Before your renewal date your current lender will ask you to renew early. Most lenders send renewal letters out 6 months before your renewal date, and then again at 4 months. They’ll offer you a new rate which, while slightly lower than their current available rate, is typically not the best rate you can get.

Remember, your current provider will often hold the rate they offer you until your renewal date, so it doesn’t hurt to shop around. If you can’t find something better, you can always accept their offer anytime before your renewal date.

Instead of accepting your current provider’s renewal offer straightaway, start comparing rates from other providers and mortgage brokers to see what else is available. You should begin shopping four months before your renewal date to give yourself the time to switch, if needed.

Advertisement

While there are no penalties for switching providers, there may be some fees involved. Many of these fees will often be covered by your new provider. You will also need to requalify but this isn’t something you should worry too much about. It’s usually easier to requalify at renewal time so long as you remain employed and your income hasn’t decreased. However, if your financial situation has recently worsened, it’s possible you won’t qualify for a better rate than your renewal offer. If this is the case, it may be best to renew with your existing provider.

In any case, comparing available rates and switching providers is easier with help from a mortgage professional such as a mortgage broker. Getting expert advice is never a bad idea and, in the case of mortgage brokers, consultations are free.

Advertisement

4. Use a mortgage renewal rate hold

A rate hold lets you secure a mortgage rate well before your renewal date. Rate holds normally last 90 to 160 days. This lets you compare rates several months before your renewal date, giving you time to find the best deal.

Let’s say you find a great rate four months before your renewal date. You can apply for that rate today and, if you’re approved, hold that rate until your renewal date. If rates go up during the rate hold period, the lender will still honour the original rate you were approved. If rates go down, you can still negotiate for a lower rate. This is why it’s important to start shopping around months ahead of your renewal date.

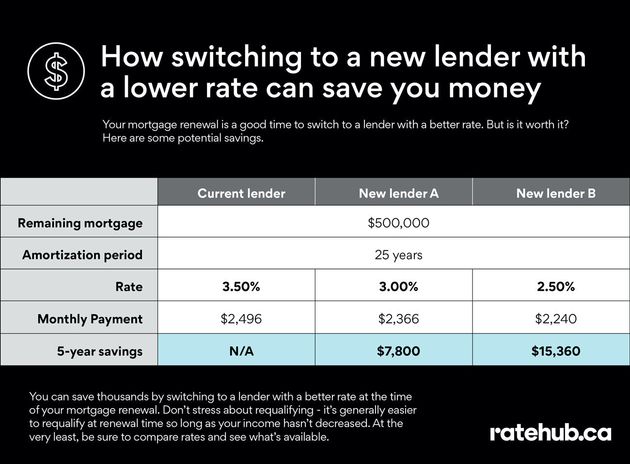

Don’t be afraid to switch lenders, especially if you can get a better rate. A better deal on your mortgage can save you thousands of dollars. Here’s a quick example:

In this example, even half a percent off your interest rate can save you around $130 a month — that’s an extra $7,800 over a five-year term.

Remember, switching lenders isn’t the same as refinancing, but it does require you to requalify with your new lender. With that in mind, here are three important points to consider:

- Leave enough time: Start your application at least two to four months before your renewal date.

- Don’t stress about requalifying: Consider that most people’s incomes go up over time, and that your mortgage balance should have been going down because you’ve been making regular payments. Your financial position at renewal time is therefore often better than when you first got your mortgage. That means requalifying shouldn’t be an issue, assuming your employment and financial situations haven’t deteriorated.

- Ask about fee waivers: Many mortgage fees can be waived or can be covered by your lender if you ask.

6. Should you refinance your mortgage?

If you want to access some of your home equity, consolidate your debts, or change any part of your original mortgage, you could consider refinancing. Luckily, your renewal date is the best time to refinance.

As mentioned, there are lots of reasons why you might refinance, and it’s a big decision. Before you bite the bullet, you should learn more about what a mortgage refinance is all about, and speak to a mortgage professional to understand your options.

The bottom line

Mortgage renewal time is the perfect opportunity for you to choose a mortgage that better suits your current financial situation and needs. It’s a great time to shop around and save money by obtaining a lower rate. It’s also the best time to refinance your mortgage if you need to take out money from your home, consolidate your debts or change any other part of your original mortgage.

To capitalize on the opportunity to improve your mortgage, start comparing rates at least four months before your renewal date. This gives you time to find a better offer, get advice and switch to a new lender (or even refinance), if that better suits your needs. Whatever your decision, being smart and prepared will set you up for success.

Call Lakhvinder Gill – (604) 725-6734

For your Free Insurance Consultation or Email Us: [email protected]